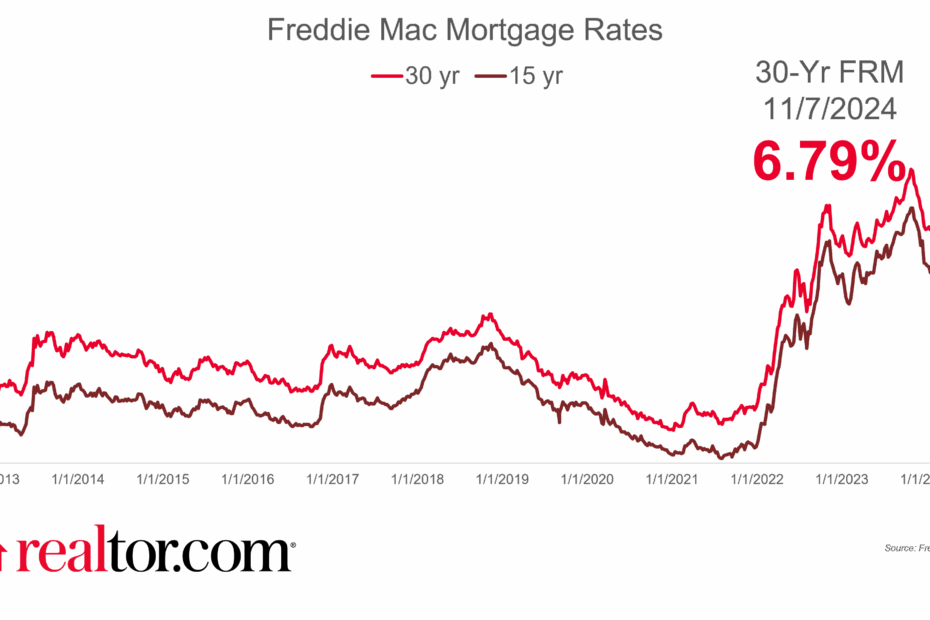

Current Mortgage Rates 2025

Reddit users are particularly focused on the current state of mortgage rates, especially for 30-year fixed loans. According to recent data, the average 30-year fixed mortgage rate sits at 6.79% as of June 2025, with 15-year fixed rates averaging 5.94%. However, these national averages don’t tell the whole story.

Redditors report significant variations between lenders, with differences of up to 0.5 percentage points for identical loan scenarios. One user shared: “I was quoted 6.5% by a major bank but found 6.1% with a local credit union for the exact same loan amount and term.”

How Credit Scores Impact Your Rate

| Credit Score Range | Average 30-Year Rate (June 2025) | Rate Difference vs. Excellent Credit |

| 760+ (Excellent) | 6.32% | — |

| 700-759 (Good) | 6.57% | +0.25% |

| 660-699 (Fair) | 6.89% | +0.57% |

| 620-659 (Poor) | 7.24% | +0.92% |

Credit score remains one of the most significant factors affecting your mortgage rate. Reddit discussions reveal that borrowers with scores above 760 are securing rates approximately 0.92 percentage points lower than those with scores in the 620-659 range. This difference can translate to thousands of dollars over the life of a loan.

Securing No-Points Rates in a Volatile Market

A recurring theme in Reddit threads is the confusion around discount points. Many lenders advertise attractive rates that require purchasing points—essentially prepaying interest to lower your rate. One Redditor noted: “The 5.9% rate I saw advertised actually cost 2 points, which was $8,000 on my loan amount. The no-points rate was 6.4%.”

Compare Today’s Mortgage Rates

See personalized rates from multiple lenders without affecting your credit score.

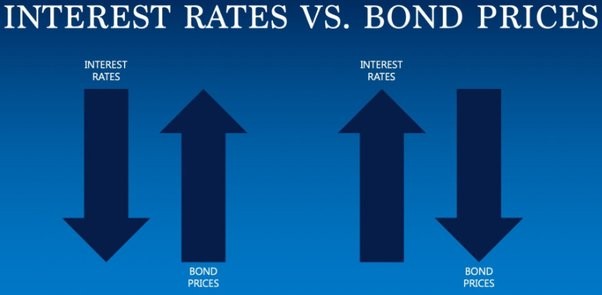

Fixed vs. Variable Rates: Understanding Bond Yields

Reddit’s mortgage communities have been buzzing about the relationship between bond yields and fixed mortgage rates. Unlike variable rates, which follow central bank decisions more directly, fixed mortgage rates are primarily influenced by the 10-year Treasury yield.

As one financial advisor on Reddit explained: “The 10-year Treasury yield has more impact on your 30-year fixed mortgage rate than any Fed announcement. When yields rise, fixed mortgage rates typically follow within days.”

“I locked in a 6.25% 30-year fixed rate last week after watching the 10-year Treasury yield drop 15 basis points. My lender explained that the mortgage market was pricing in future Fed cuts, even though none had happened yet.”

Why Shorter-Term Fixed Mortgages Are Gaining Popularity

The spread between 30-year and 15-year fixed rates has widened to nearly 0.85 percentage points in 2025. This significant difference has led many Reddit users to consider shorter-term mortgages as a hedge against uncertainty.

A 15-year fixed mortgage at 5.94% not only offers a lower rate but also builds equity faster. However, the tradeoff is higher monthly payments. For a $300,000 loan, the difference in monthly payment between a 30-year and 15-year term is approximately $650.

Some Reddit users are also exploring hybrid options like the 20-year fixed mortgage, which offers a middle ground between the 30-year and 15-year terms. Current 20-year fixed rates average around 6.46%, providing a balance between payment affordability and faster equity building.

Find Your Ideal Mortgage Term

Compare 15-year, 20-year, and 30-year fixed rates from top lenders.

Refinancing Strategies: Rate Buy-Downs vs. Waiting

#image_title

Refinancing dilemmas dominate Reddit discussions, with users debating whether to pay for rate buy-downs or wait for potentially lower rates. The 2-1 buydown has emerged as a particularly hot topic, with mixed opinions on its value.

Understanding the 2-1 Buydown

A 2-1 buydown temporarily reduces your interest rate by 2% in the first year and 1% in the second year before returning to the standard rate in year three. Reddit users report that sellers are increasingly offering to cover buydown costs as a concession in cooling markets.

| Year | Standard Rate | 2-1 Buydown Rate | Monthly Savings on $400,000 Loan |

| Year 1 | 6.75% | 4.75% | $456 |

| Year 2 | 6.75% | 5.75% | $233 |

| Year 3+ | 6.75% | 6.75% | $0 |

The cost of a 2-1 buydown typically ranges from 2-3% of the loan amount. Reddit users debate whether this upfront cost is worth the temporary savings, especially if rates drop enough to refinance in the near future.

Hidden Fees in “Free” Refinance Offers

Reddit threads have been warning about “no-cost” refinance offers that actually roll fees into the loan or charge a higher interest rate. One user shared: “I was offered a ‘free’ refinance that had no closing costs, but the rate was 0.375% higher than their standard offer. Over 30 years, that’s far more expensive than paying closing costs upfront.”

When Refinancing Makes Sense

- You can reduce your rate by at least 0.75%

- You plan to stay in your home for 5+ years

- You can recoup closing costs within 3 years

- You need to tap equity for major expenses

- You want to eliminate PMI payments

When to Avoid Refinancing

- Rate reduction is less than 0.5%

- You plan to move within 2-3 years

- Closing costs exceed potential savings

- You’ve already paid many years on current loan

- Your credit score has decreased significantly

Calculate Your Refinance Savings

See if refinancing makes financial sense for your situation.

First-Time Homebuyer Guide: Low Down Payment Options

First-time homebuyers on Reddit are particularly concerned about navigating the mortgage process with limited savings for down payments. Discussions frequently center around low-down-payment options and avoiding private mortgage insurance (PMI).

Low Down Payment Loan Options

FHA Loans

3.5% down payment with credit scores 580+

10% down with scores 500-579

Mandatory mortgage insurance

Higher debt-to-income ratios allowed

Conventional 97

3% down payment option

Minimum credit score of 620

PMI can be removed at 20% equity

First-time buyer friendly

VA Loans

0% down payment for eligible veterans

No mortgage insurance required

Competitive interest rates

Flexible credit requirements

Reddit users report varying experiences with these programs. One first-time buyer shared: “I went with the Conventional 97 because even though FHA had slightly lower rates, the ability to drop PMI later saved me thousands in the long run.”

Preapproval vs. Prequalification: What Reddit Users Learned

A common point of confusion among Reddit’s first-time homebuyers is the difference between prequalification and preapproval. Prequalification is a quick estimate based on self-reported information, while preapproval involves verification of income, assets, and credit.

Experienced Redditors consistently advise getting fully preapproved before house hunting. As one user put it: “In this competitive market, sellers won’t even look at offers without a solid preapproval letter. My prequalification letter was worthless when making offers.”

“I got preapproved with three different lenders and their rates varied by 0.4%. Shopping around saved me $100 per month on my mortgage payment.”

Get Preapproved Today

Start your homebuying journey with a solid preapproval letter.

Mortgage Affordability: What Lenders Actually Look At

Reddit discussions reveal significant confusion about how lenders determine mortgage affordability. While many users focus solely on income, lenders evaluate multiple factors when calculating how much you can borrow.

Debt-to-Income Ratio: The Critical Number

The most discussed affordability metric on Reddit is the debt-to-income (DTI) ratio. Most conventional lenders cap this at 43%, though some loan programs allow up to 50%. This means your total monthly debt payments, including your new mortgage, shouldn’t exceed these percentages of your gross monthly income.

| Gross Annual Income | Maximum Monthly Debt (43% DTI) | Existing Monthly Debt | Available for Mortgage Payment | Approximate Loan Amount (6.75%, 30yr) |

| $75,000 | $2,688 | $500 | $2,188 | $337,000 |

| $100,000 | $3,583 | $800 | $2,783 | $429,000 |

| $150,000 | $5,375 | $1,200 | $4,175 | $644,000 |

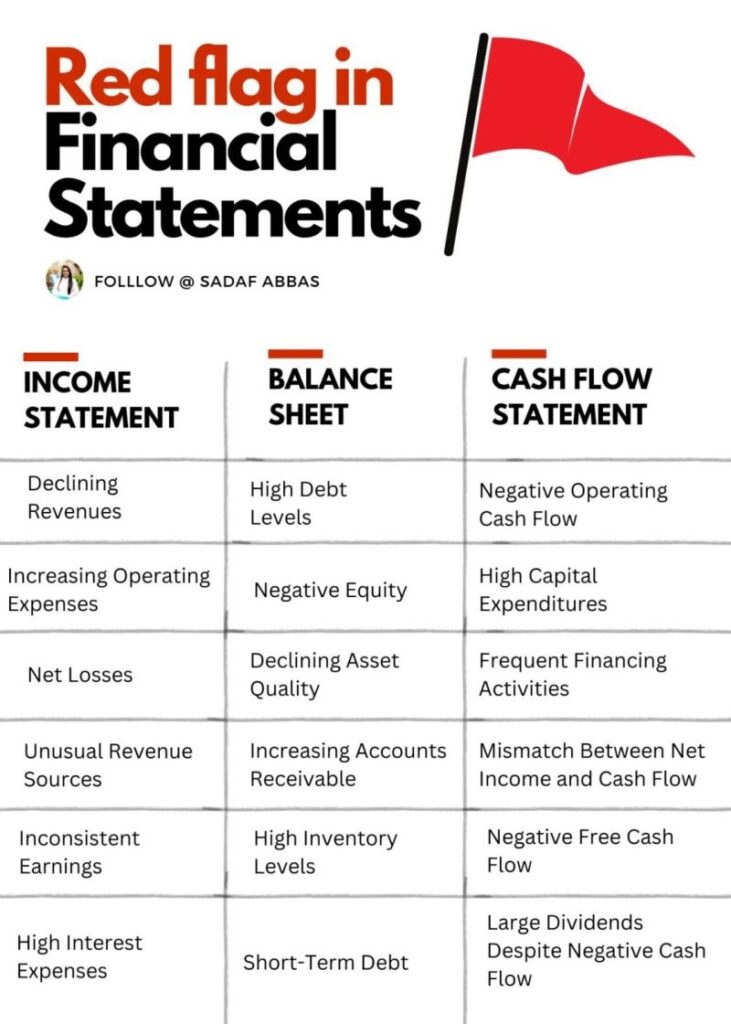

Bank Statement Scrutiny: What Raises Red Flags

Reddit threads reveal increasing lender scrutiny of bank statements. Users report lenders flagging specific transaction types that could jeopardize approval:

Transactions That Concern Lenders

- Frequent gambling transactions (even small amounts)

- Buy-now-pay-later (BNPL) payments

- Unexplained large deposits

- Regular overdraft fees

- Transfers to crypto exchanges

How to Prepare Your Finances

- Clean up statements 3-6 months before applying

- Document all large deposits with clear sources

- Minimize use of BNPL services

- Avoid gambling transactions entirely

- Maintain consistent income deposits

One Reddit user shared: “My lender questioned a $200 monthly payment to Afterpay and required a letter explaining all my BNPL accounts. They calculated these payments into my DTI even though they didn’t show on my credit report.”

Check Your Mortgage Affordability

Get a personalized assessment of how much home you can afford.

Economic Shifts and Their Impact on Mortgage Rates

Reddit’s financially-savvy users are closely monitoring economic indicators that influence mortgage rates. Bond yield spikes, Federal Reserve policy changes, and inflation reports are frequent topics of discussion.

Bond Yields: The Leading Indicator

The relationship between 10-year Treasury yields and mortgage rates is a recurring theme in Reddit discussions. When yields rise, mortgage rates typically follow. Recent volatility in the bond market has created uncertainty in mortgage rate forecasts.

As one financial analyst on Reddit explained: “The spread between the 10-year Treasury yield and 30-year mortgage rates has been wider than historical norms throughout 2025. This suggests potential for rates to compress if market conditions normalize.”

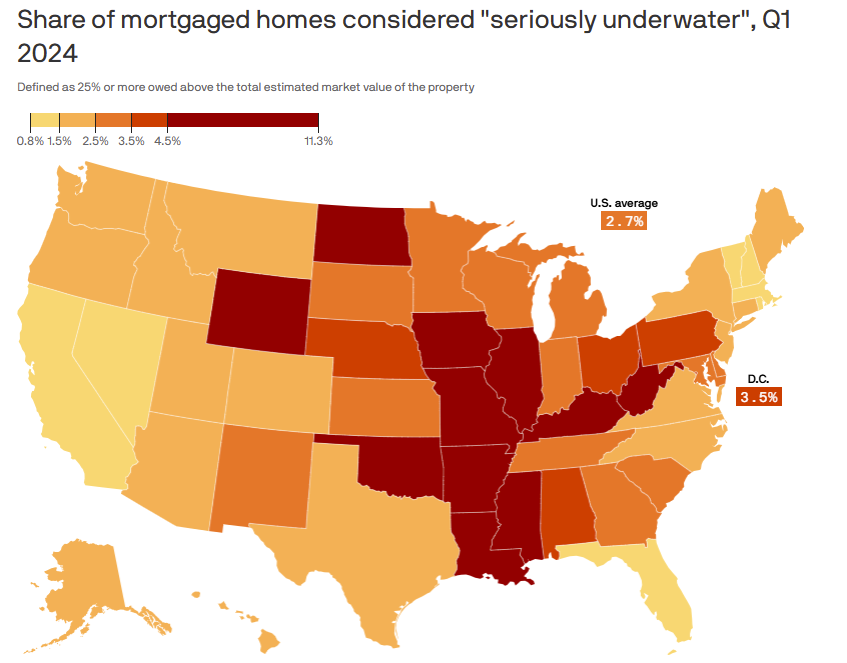

The Rise of Underwater Mortgages

Reddit users in certain markets report increasing concerns about negative equity. With home prices stabilizing or declining in some regions while mortgage rates remain elevated, some recent buyers find themselves owing more than their homes are worth.

This trend is particularly pronounced in markets that saw rapid price appreciation during 2021-2023. One Redditor shared: “I bought in Phoenix in 2022 at the peak. My home has lost 12% of its value while my neighbor just refinanced into a higher rate to get out of an ARM.”

Declining Demand and Affordability Challenges

Multiple Reddit threads discuss the relationship between high mortgage rates and declining housing demand. With the average 30-year fixed rate hovering near 6.8%, many potential buyers have been priced out of the market.

“My budget allowed for a $500,000 home when rates were 3%. At today’s rates, I can only afford $350,000 for the same monthly payment. There’s nothing available in my area at that price point.”

This affordability squeeze has led to reduced transaction volume, with some sellers reluctant to list their homes due to the “rate lock” effect—they don’t want to give up their existing low-rate mortgages.

Stay Informed on Rate Trends

Get weekly updates on mortgage rates and economic factors.

When to Lock In Your Rate: Expert Advice

The question of when to lock in a mortgage rate dominates Reddit discussions. While timing the market perfectly is impossible, experts and experienced Redditors offer several guidelines:

Lock If You’re Within 60 Days of Closing

The risk of rates rising exceeds the potential benefit of them falling further. Most rate locks are free for 30-60 days, providing valuable certainty.

Consider Float-Down Options

Some lenders offer “float-down” provisions that allow you to secure a lower rate if rates fall during your lock period, typically for a fee of 0.5-1% of the loan amount.

Watch Weekly Trend Patterns

Reddit users have observed that rates often dip mid-week (Tuesday-Wednesday) and rise toward the end of the week as lenders manage their pipelines.

Lender Comparison Checklist

Based on Reddit’s collective wisdom, here’s a checklist for comparing mortgage offers:

- Compare the APR, not just the interest rate (APR includes most fees)

- Request Loan Estimates from at least three lenders for accurate comparison

- Identify all lender fees, including origination, application, and underwriting

- Check for prepayment penalties or early payoff fees

- Evaluate rate lock policies and extension fees

- Research lender reviews specifically for communication during closing

- Ask about relationship discounts for existing banking customers

The mortgage landscape in 2025 continues to evolve, with rates remaining historically moderate but significantly higher than the record lows of 2020-2021. By staying informed about economic trends, understanding your personal affordability metrics, and strategically timing your rate lock, you can navigate this complex market successfully.

Ready to Move Forward?

Compare personalized mortgage rates from top lenders and lock in your rate today.