Uncategorized

Elementor #2850

1031 Exchange and Inherited Property: What Arizona Heirs Need to Know | Todd Uzzell Mortgage 1031 Exchange and Inherited Property:

What is a Home Equity Loan and How Does It Work

What Is a Home Equity Loan and How Does It Work? | Todd Uzzell Mortgage What Is a Home Equity

What Is a Mortgage? A Complete Guide for Homebuyers

Stepping into the world of homeownership begins with understanding what a mortgage is and how it works. Whether you’re a

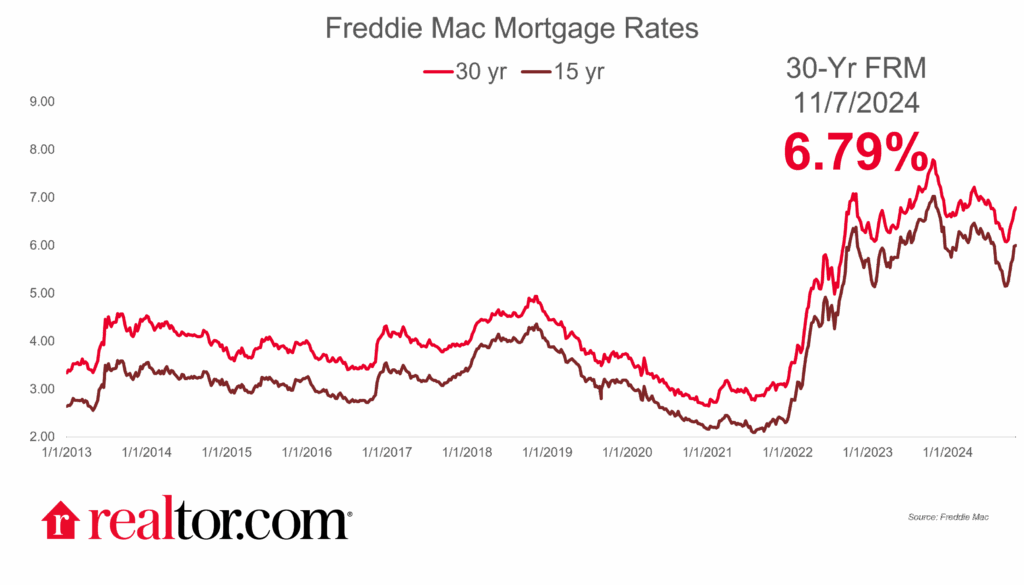

2025 Mortgage Rates: Reddit’s Top Questions & Expert Insights

Explore 2025 mortgage rates 2025 through Reddit’s most-asked questions. Get expert insights on fixed vs. variable rates, refinancing strategies, and economic impacts on the housing market.

How to Pay Off Your Arizona Mortgage in 5-7 Years (Proven Strategies!)

Discover proven strategies to pay off your Arizona mortgage in 5-7 years. Learn how to accelerate debt repayment and become mortgage-free faster.

Understanding Mortgages: A Complete Guide for Homebuyers

Stepping into the world of homeownership begins with understanding mortgages – the financial vehicles that make buying a home possible

Navigating the Mortgage Loan Process in Phoenix

Navigating the Mortgage Loan Process in Phoenix: A Step-by-Step Guide Buying a home is a major milestone, and the mortgage

Why Mortgage Pre-Approval is Essential for Homebuyers

Why Mortgage Pre-Approval is Essential for Phoenix Homebuyers Introduction Buying a home in Phoenix is an exciting journey, but without