If you’ve been watching mortgage rates this year and wondering why they wiggle up and down even when the headlines sound okay, you’re definitely not alone. As a local mortgage lender in Phoenix, I hear this question from first-time buyers, move-up families, veterans, retirees, and investors almost every week.

The truth is, how mortgage rates are determined in 2026 isn’t controlled by one bank or person. It’s a combination of big-picture economic forces, investor sentiment, and your own financial situation. Understanding the real drivers can take a lot of the mystery (and stress) out of buying, refinancing, or building a new home in the Valley.

Let’s walk through it in plain, straightforward language — like we’re sitting down for coffee.

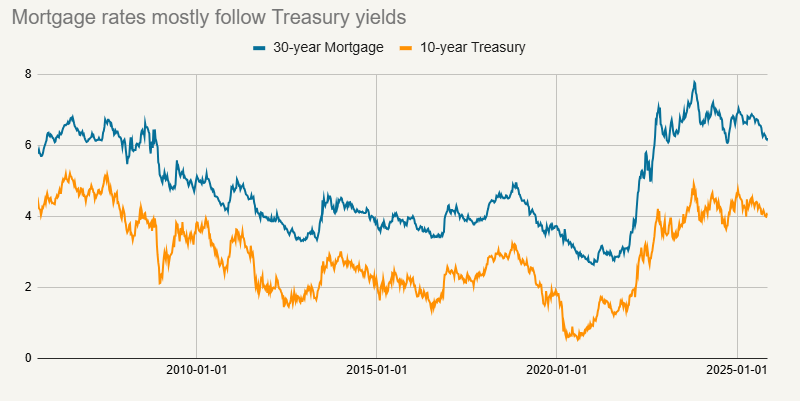

The Main Driver: The 10-Year U.S. Treasury Yield

The biggest influence on 30-year fixed mortgage rates (the loan most people use) is the yield on the 10-year U.S. Treasury note. Lenders use this as a benchmark for long-term borrowing costs.

When investors buy or sell these government bonds, the yield moves — and mortgage rates usually follow within a day or two. In early April 2026, the 10-year Treasury yield has kept 30-year fixed rates in Arizona hovering roughly between 6.13% and 6.45%, depending on the lender and your credit.

Higher yields (often triggered by concerns about inflation or strong economic growth) push mortgage rates up. Lower yields pull them down. It’s not a perfect one-to-one match, but the connection is very strong.

The Federal Reserve’s Influence (Indirect but Important)

Many people assume the Fed sets mortgage rates directly. They don’t. The Fed controls the short-term federal funds rate (currently in the 3.5%–3.75% range as of late March 2026). This affects the broader economy, but your 30-year mortgage rate tracks the 10-year Treasury more closely.

Still, Fed signals matter a lot. When the Fed hints at future rate cuts or holds steady to fight inflation, it can calm or stir the bond market and move mortgage rates accordingly. Right now in 2026, the Fed continues to watch inflation closely. Sticky inflation keeps rates from dropping quickly; cooling economic data could open the door for modest relief later this year.

Other Important Factors Shaping Rates in 2026

Several other pieces complete the picture of how mortgage rates are determined in 2026:

- Inflation Reports: Faster-than-expected price increases make investors demand higher returns, lifting rates.

- Economic Data: Jobs reports, GDP growth, and consumer spending numbers can swing yields quickly.

- Global Events: Geopolitical issues, energy prices, or international market moves often cause sudden shifts.

- Mortgage-Backed Securities: Big investors buy bundles of home loans. If they see more risk, they want higher yields — which means higher rates for borrowers.

- Your Personal Profile & Lender Pricing: Credit score, down payment, debt-to-income ratio, loan type (conventional, FHA, VA, jumbo), and even the property location all affect the final rate you’re offered. Shopping multiple lenders can easily save 0.25%–0.50% or more.

As of early April 2026, 30-year fixed rates in the Phoenix area are averaging around 6.13%–6.875% APR, with some lenders offering better pricing for strong credit or specific programs.

What This Means for Phoenix-Area Buyers and Homeowners

Different situations call for different approaches:

- First-time buyers: Rates in the low-to-mid 6% range make budgeting essential. Our how much house can I afford calculator helps you see realistic payments and explore FHA options with lower down payments.

- Move-up families: Equity from your current home can offset rate differences. Seller concessions or temporary buydowns are still common in competitive Valley neighborhoods.

- Veterans: VA loans often feature competitive rates and zero down payment. Visit our VA loans page to see how they perform right now.

- Retirees: Stable payments matter. Strategic refinancing or timing your next move can protect your budget.

- Investors and new-build clients: Higher-price or construction projects may use jumbo or specialized financing. Builder incentives can help soften the impact of rates.

The encouraging part? Rates have been more stable in 2026 than in some previous years, and small improvements or lender credits can still create meaningful savings.

Smart Tips to Get the Best Rate Possible

Here’s what actually helps in today’s environment:

- Improve your credit score before applying — even 20–30 points can lower your rate.

- Get pre-approved early so you know your real buying power. Start here: Mortgage Pre-Qualification.

- Compare offers from multiple lenders — fees and pricing vary more than most people realize.

- Ask about rate buydowns or lender credits, especially on new construction in areas like Gilbert, Queen Creek, Surprise, or Buckeye.

- Watch key dates — major economic reports and Fed meetings can move rates. We can help you decide when to lock.

Looking Ahead for the Rest of 2026

Most experts expect 30-year fixed rates to stay in a 5.9%–6.5% range through 2026, with possible modest declines if inflation continues to ease and the Fed cuts further. Bond markets can shift fast, so nothing is guaranteed — but knowing how mortgage rates are determined in 2026 helps you plan instead of just reacting to headlines.

In the Phoenix housing market, prepared buyers who understand these dynamics are still finding solid opportunities.

Q&A – Common Questions About Mortgage Rates in 2026

Q: Why does my quoted rate change day to day? A: Small daily movements in the Treasury yield and bond market cause normal fluctuations. We can lock a rate when the timing works for your goals.

Q: Are rates likely to drop below 6% this year? A: It’s possible later in 2026 if data supports it, but many forecasts see the mid-6% range as more realistic near-term. Focus on overall affordability and the right home rather than waiting for perfection.

Q: Does the Fed directly control my mortgage rate? A: No — they influence the economy and short-term rates, but your long-term mortgage follows the 10-year Treasury more closely.

Q: Should I buy now or wait for lower rates? A: It depends on your timeline, local inventory, and the specific home. Many clients are moving forward successfully by combining current rates with negotiating power or incentives.

Ready to Put This Knowledge to Work for Your Situation?

Understanding how mortgage rates are determined in 2026 is useful, but applying it to your goals is what counts. Whether you’re buying your first home in Mesa, moving up in Scottsdale, using VA benefits, retiring in Chandler, investing, or building new in the West Valley, I can give you clear, no-pressure guidance.

Let’s review your numbers together, run scenarios with our calculators, and build a plan that fits today’s rates and the Phoenix market.

Contact me today to schedule a quick call or start pre-qualification. Visit todduzzell.com/contact-us/ or reach out directly 480-330-1724— I’m here to help Arizona families finance homes with confidence, one straightforward conversation at a time.

Todd Uzzell Your Local Phoenix Mortgage Expert Serving the entire Valley — from first-time buyers to seasoned investors.